OCEAN SPRINGS — Nita Hope, 62, has lived in the same home since 1990.

Now, she’s boxing up her life, painting the walls and putting it up for sale.

“Because what we’re paying in insurance is equal to our mortgage every month,” she said. “Frankly, when you’re retired, budget is tight … we couldn’t keep it up. So, I don’t know exactly what I’m going to do, but I am going to leave Mississippi. I’m going to go north.”

A rise in homeowners insurance costs along the Mississippi Gulf Coast — especially for policies that include wind coverage — continues to strain residents’ finances.

According to Insurance.com, the average cost of homeowners insurance for a $300,000 home in Mississippi is $3,380 per year — higher than the national average of $2,601. Gautier has the state’s highest average at $7,816. In Ocean Springs, where Hope lives, the average is $6,295.

For many retirees, insurance feels inescapable. Those with mortgages must carry homeowners and wind insurance. Residents in flood zones are also often required to have flood insurance. Hope said that in 2019, she paid $6,200 for all three policies. That cost has now risen to nearly $10,000.

“I don’t know what I was hoping for, to be honest — a rebate? It was a fantasy,” she said. “I somehow thought … somebody would finally intervene … it’s very clear that we are absolutely powerless.”

Nonrenewals grow on the Gulf Coast

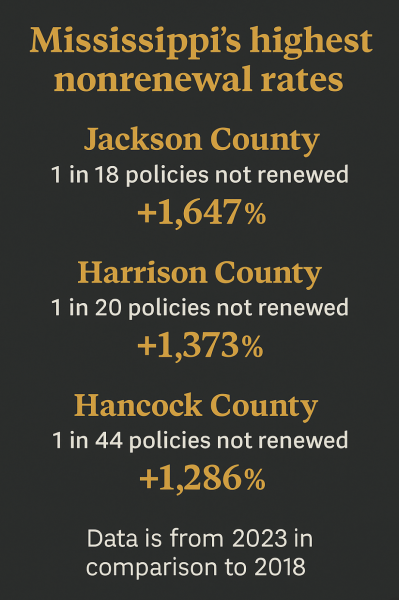

Many Mississippians are now opening mailboxes to find letters of “nonrenewal,” as companies drop policies to reduce liability. According to The New York Times, Mississippi ranked sixth in the nation for nonrenewals in 2023, with one out of every 67 policies not renewed.

“Without insurance, you can’t get a mortgage; without a mortgage, most Americans can’t buy a home,” the Times report noted. “Communities that are deemed too dangerous to insure face the risk of falling property values, which means less tax revenue for schools, police and other basic services.”

Mark E. Strickland with SouthGroup Insurance Services said fallout from storms like hurricanes Laura and Ida in 2020 and 2021 led many companies to stop writing wind insurance on the Gulf Coast.

“There’s fewer companies writing — our population is increasing — and so it’s supply and demand,” he said. “The number of carriers that would write a homeowner (policy) with wind has dwindled, the companies that remained and were actively writing said, ‘Look, we’re taking on more risk. We’re going to raise our rates.’”

Strickland said the trend has begun to level off this year, with nonrenewals slowing and some companies re-entering the market.

“Post-2020 and 2021 hurricane seasons, you did see just companies leaving the area en masse … but that is slowing down for sure,” Strickland said. “The outlook is certainly better than it was two years ago, when we were having double-digit inflation.”

Rising rebuild costs

Even outside of wind coverage, inflation in replacement costs has driven up insurance rates. A home that cost $200,000 to replace in 2019 might now cost $300,000.

Strickland said wind coverage alone can account for 70% of a homeowner’s insurance premium in south Mississippi. When private options disappear, many homeowners turn to the Mississippi Windstorm Underwriting Association — known as the wind pool.

The state wind pool provides residents and business owners with a reliable market for wind insurance in in Hancock, Harrison, Jackson, Pearl River, Stone and George counties. Wind pool premiums are more than those offered by the private market and are usually a last resort for consumers.

There are two types of insurance carriers: admitted and nonadmitted. Admitted carriers — like State Farm or Nationwide — are approved by the Mississippi Insurance Department and backed by the state’s guarantee fund.

Nonadmitted carriers do not have to get state approval to raise rates. They often offer lower premiums but come with fewer protections if they fail to pay out.

“People have hopes and dreams and aspirations: ‘Well, this is a nonadmitted company, and they’ve only been in business for six years. Take it or leave it, but it’s $1,000 cheaper.’ They usually take it,” Strickland said. “Sometimes, it’s just the only option, or it’s very much the best option.”

Some insurers raise rates dramatically instead of sending cancellation notices — pushing customers to drop coverage.

Hope said she chose the wind pool because it felt more reliable.

“I’m paying a lot extra … because I’m gambling that they won’t try to slide out from under the mandate (to pay in the event of mass damages) … versus these guys that may sell it to me cheaper, but there’s no oversight,” she said.

How upgrades, income and state programs intersect

Strickland said mitigation measures like impact glass or fortified roofs help make homes more insurable, but retrofitting older homes is often too expensive to justify premium discounts.

“Fixed income and lower income people have really, absolutely been hurt by this … If inflation keeps going and the stock market goes crazy, then that’s very scary to a lot of people,” he said.

Very few admitted companies write wind coverage within a half mile of the water edge, except for nonadmitted surplus lines carriers whose premiums have increased over 50% in the last two years, the Mississippi Insurance Department stated. The department is working to recruit more companies to write wind insurance in the area.

To help curb premiums, the insurance department launched Strengthen Mississippi Homes, offering $10,000 grants to homeowners in six counties, including Pearl River, Stone, George, Hancock, Harrison and Jackson.

Four homes have been upgraded so far this year in a pilot program. A proposal to expand the program didn’t pass.

“We had an agreement … we would get $5 million,” said state Insurance Commissioner Mike Chaney. “That’s 1,000 (fortified) homes a year.”

He hopes to see expansion of a mitigation program, as neighboring states have done, in order to avoid a future without insurance availability for Mississippi residents. The department hopes to fully launch the current program this summer. Officials have already seen more than 1,100 applicants.

Chaney recently approved a 16% increase in wind pool premiums to be fully instituted by 2027— the first increase since the late 2000s. The increase is still under review.

He said the biggest rate increases have come from nonadmitted carriers.

“When somebody says, ‘Rates out of sight on the Gulf Coast,’ I say, ‘Prove it,’” he said. “The rates … are what we call nonadmitted companies, and those are surplus lines. If they go under, you lose your money because … they don’t pay into a guarantee fund.”

He said the number of policies from nonadmitted companies has increased from 8% to 10% in the past three years.

Chaney said many insurers won’t cover older roofs or may only offer depreciated value.

“I had one yesterday … They said, “We’re not going to write your roofs at over 10 years old … If that tree isn’t cut in two weeks, we’re not going to renew you.’ Now, you can’t do that to homeowners, but they do it,” Chaney said. “I can’t kick them out of the state because they have a little business, but I threatened to say, ‘You can’t write any more insurance until you fix the problems.’”

He said nonrenewals aren’t always a negative, and that the number of uninsured homeowners in Mississippi did not see a significant change despite the high nonrenewal rate.

“It means that people said to their carrier, ‘Look, you’re too high on your premium — we can get a better deal over here,’” Chaney said.

There were 13,936 policies under the wind pool as of April 1, 2024, a decrease from the previous year. Chaney said the number has not changed much since then, and that the price of the wind pool to consumers has not seen a large increase.

Chaney said as availability of insurance increases, he can use it as leverage to protect consumers. He encouraged homeowners to contact the Mississippi Insurance Department if they experience unfair treatment.